#TheCBNFiles: Making Money to Spend Money

This week on 1914 Reader, we are publishing a series of posts on the recently released financial statements of Nigeria’s Central Bank. This will be a mixture of analysis, opinion and guest posts. There is a lot of information in the accounts and we don’t believe that a single post can do justice to them.

A Quick Recap

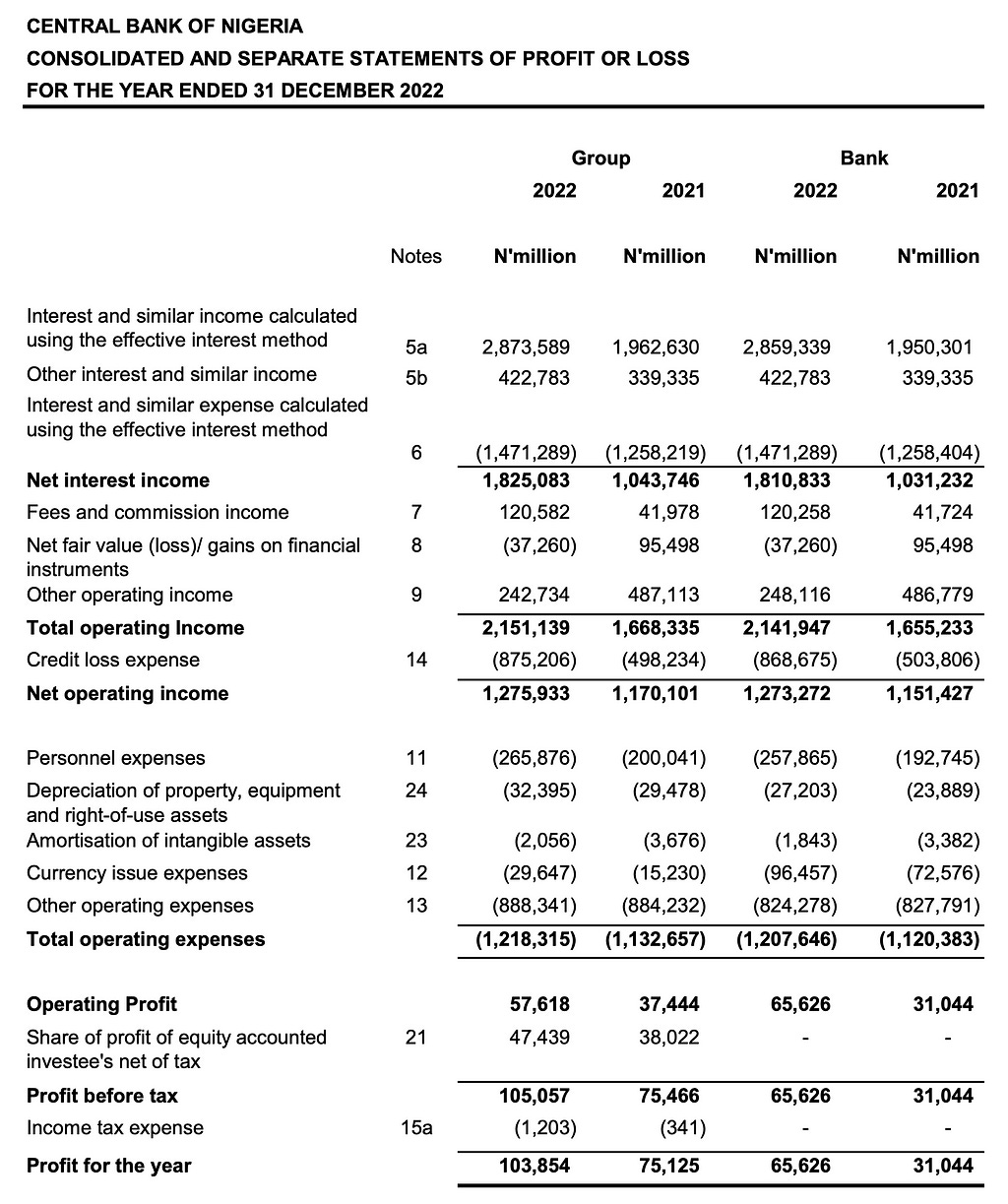

We established in the first post about spending that CBN needed to earn money to cover the more than N2 trillion hole made by expenses and accounting charges in its accounts. To oversimplify; the CBN got involved in some lending and ended up losing N875 billion. It also got involved in forex activities and blew a N848 billion hole in its accounts (N346 billion in unrealised losses on forex holdings and N156 billion on rebates trying to attract dollars into the economy).

Everything else looks small compared to these lending and forex activities (the famous ‘interventions’ that generate so much press coverage only cost N125 billion in the grand scheme of things).

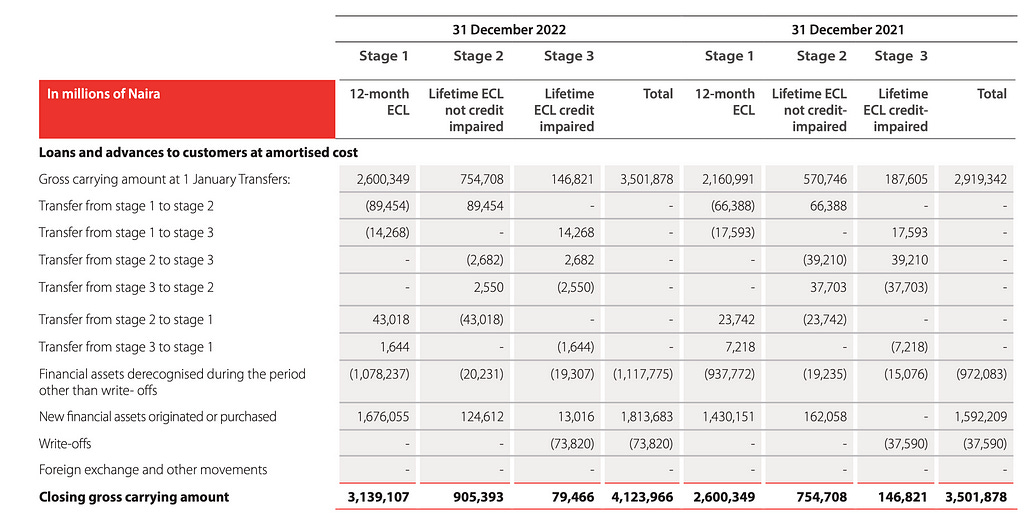

Given how much CBN managed to lose doing ‘lending’, the question needs to be asked whether CBN’s mandate ought to be redefined to remove it from doing these things which its clearly not good at. Is CBN a good lender if it managed to write off more than N700 billion as Stage 3 credit losses in 2022? For a comparison, here is Zenith Bank’s 2022 reported losses on lending:

Its Stage 3 losses are slightly more than 10 percent of what CBN lost. The immediate answer will be that CBN is not like a normal bank and therefore cannot lend in the same way. That is of course true. But it cannot keep losing money forever either.

Counting from the top

We come back to the current year and what CBN earned:

As we can see, the chunk of income that CBN made really comes down to one thing: interest income. And it is probably worth noting that had the CBN earned the same amount in 2022 as it did in 2021, it would have made a loss large enough to wipe out all of its reserves. But that is merely a thought experiment.

Fair Value

Let’s start with the smaller amount first — N422 billion in Other interest and similar income:

FVTPL stands for Fair Value Through the Profit and Loss. To explain in simple language: under IFRS (the rules that govern how you prepare your accounts), certain financial assets have to be measured at ‘fair value’. This means that if you own an asset like a stock or a bond and there is a market where that asset is traded publicly and in an orderly manner i.e. a stock exchange or bond market, you have to record the value of that asset in your books based on what you would get if you were to sell it in that public and orderly market.

So say I own one Apple share and on 31 December 2022 (the date at which I prepared my accounts), it was trading for $1,000 on the stock exchange, I will record $1,000 in my accounts as the fair value of the asset as at the date of my accounts. But you are probably thinking that the value of assets traded in public and orderly markets are always moving up and down. Yes, and that is where FVTPL comes in: it is how we measure changes in the fair value of assets from one period to the next in the accounts. If at the end of 2023, the Apple share is valued at $1,200, I will record $200 in the Profit and Loss as a gain. If it was to drop in value to $750, I will record $250 as a loss. The asset itself sits on my balance sheet (I have not sold it) but the movements in its fair value are recorded in the P&L i.e. FVTPL. This concept is useful as it's something we will come across multiple times. You will notice that a lot of things in IFRS accounting work in this way — recall that N346 billion was recorded as unrealised losses on forex in the same accounts following a similar principle.

So in this case, the N422 billion is the movement on the assets (foreign securities) that the CBN owns. That’s a lot and you imagine that to make N422 billion, you are probably carrying quite a large amount of said securities. If we go hunting for the assets themselves, we see these:

We can say that it earned that N422 billion on the N3.9 trillion of Debt securities held at FVTPL (Amortised cost is a separate way of measuring assets i.e. the same asset cannot be recorded at Fair Vaue and Amortised Cost). I don’t have any insight into what these particular debt securities are but I can say that, in general, debt securities held at FVTPL are typically things like bonds and debentures.

I should say that the overall quality of the CBN’s financial statements are very poor both from an aesthetic point of view (it looks like something that was done on a word document and then ‘saved as PDF’) and the actual quality of the disclosures. When you consider that 8 years worth of accounts running to well over a thousand pages were dumped on the public literally late at night, a quote from Winston Churchill (possibly apocryphal) is what comes to mind — This report, by its very length, defends itself against the risk of being read. There is no serious attempt to really explain figures and the idea seems to be to overwhelm you with so much information that you give up and move on to something else like Big Brother Nigeria.

The Big Kahuna

Let’s move to the really big source of income — N2.8 trillion in interest income. To stress, this was the difference maker in the CBN’s accounts that allowed it to cover the expenditure in its P&L. It’s worth pointing out that the exchange rate used for the accounts (i.e. at the end of 2022) was N462 to $1:

That works out at $6.2 billion that the CBN managed to earn in interest income during 2022. That is very tasty, you will agree. And since interest is typically earned on money you lend to people, this leads us to ask a couple of questions: how much did CBN lend out and to whom did it lend it? This really is the story of the 2022 accounts and taps into what has been a topic of discussion for a number of years now.

It helps that 82 percent of the total really comes from one line — Loans and receivables so we need not disturb ourselves too much with the AMCON notes of N247 billion (what AMCON pays to CBN for money CBN paid to bailout the banks all those years) or the Federal Government Securities of N156 billion (interest CBN earned on some FG securities it owns).

Here again we see N2.4 trillion in income — the single biggest line item in the P&L — with no further breakdown and simply explained away as interest on overdraft granted to the government. But that’s enough to answer one of the questions we asked earlier — the CBN earned practically earned all of its interest income from lending to the government. The ‘overdraft’ is of course the illegal Ways & Means funding of the government that ballooned under the Buhari and Emefiele Double Act. As shown below, N4 trillion was added to the balance in 2022 alone. (The 2022 budget had a deficit of N6.2 trillion so the CBN in effect provided the bulk of the deficit financing)

The CBN said it made the interest income by charging the government an interest rate of MPR + 3%. And what was MPR?

In short, the CBN was able to earn this N2.3 trillion by charging the Nigerian government nearly 20 percent interest on the ‘overdraft’ facility it gave it. That is an eye watering amount and you must think that the government was desperate and had no other options for it to have signed up to this kind of arrangement.

Again — and I cannot stress this enough — without this interest income from lending to the government, the CBN’s account would not be able to stand on its own legs and all of its equity and reserves would be wiped out. The CBN and the Nigerian government, in this arrangement, need each other the same way a drunk man needs a lamppost i.e. not for illumination but for support.

As a famous simpleton once said — who is subsidising who?

Following the money

Now for the really controversial debate. If someone earned N2.3 trillion in interest, they must have lent out more than N10 trillion at the very least. More importantly — if the CBN lent out such a large amount of money to the government, where did the CBN find it? There are two ‘schools of thought’ on this. School 1 is what the accounts tell us and School 2 is what I will call the ‘smell test’.

Print baby, print?

Start with School 2. As the CBN did not release its accounts for years, and given that the amounts lent to the government had grown so large — N24 trillion or $53 billion — a lot of people had concluded that the CBN was simply ‘printing the money’. (Can I please urge you to remove any image of a ‘printer’ printing naira notes from your head when you hear ‘print’ in this context? It does not work like that).

I would say this was a fair assumption to make and is still so for reasons I will come to shortly. In short, the idea was that the CBN was simply electronically crediting the government’s account allowing it to spend as it needed to. In reality, the way it should work is that when a government need money and its central bank wants to fund it, the government issues bonds and the central bank buys them with newly created electronic money. The government gets cash, the central bank gets assets (bonds). This is generally not a good idea since that new money will find its way into the economy via government spending and of course lead to inflation.

Nigeria has been battling high inflation for a number of years now but the argument can be made that, as bad as Nigeria’s inflation has been, it has not yet reached anywhere near what we have seen in places like Zimbabwe where the government embarked on crazy money printing and turned the currency into toilet paper in the process.

So was the money printed or not? Hold that thought.

Sterilisation?

The other school of thought — and what the accounts strongly suggest — is that the money the CBN lent to the government was ‘sterilised’ from the banking sector. This is a silly term we like to use in finance to mean that the CBN took money out of the system to reduce the money supply. If that is the case, no new money was created as the CBN simply took out money that already existed and lent it to the government. Hence why Nigeria did not experience crazy inflation like in Zimbabwe.

Let’s step through the accounts:

The N23.3 trillion is the overdraft balance in question. The ‘ways and means’ lent to the government. We don’t need to speculate here as the CBN itself tells us so:

The two sentences above are interesting. First it tells you how or what it lends overdrafts against i.e. treasury bills and Nigerian government bonds. These are the highest quality assets out there (the Nigerian government is highly unlikely to default on its naira debts) so the suggestion here — once you read both sentences together — is that the N23.3 trillion is pretty much ‘safe’. This is further buttressed by the disclosure note below:

The overdraft to the government is classified as ‘standard grade’ and we can see that most of it is intact i.e. Stage 1 with ‘only’ N568 billion ‘spoilt’. You will also note that it is listed under ‘performing’ which means that the person the money was lent to (Nigerian government) has been repaying the loans on time and as scheduled even though the interest rate on them is almost 20 percent. This all sounds very good and nice and maybe we should just declare ‘nothing to see here’ and end this analysis.

Or maybe not. As the accounts have given us this hint, the next step is to go looking for the said assets backing the overdraft. The accounts don’t explicitly say and the best we can do is guess or try to build a case from the numbers available. Remember, we are trying to make a case here that the money was not simply ‘printed’ and was instead sourced from elsewhere.

Here is the CBN’s balance sheet:

As the name implies, it has to balance with assets equalling liabilities i.e. N58 trillion of liabilities is backed by N58 trillion of assets. We already know from looking at Note 18 earlier that the N23 trillion overdraft to the government is sitting in the Loans and receivables line of N31.4 trillion on the asset side. So we go down to the liabilities to look for the ‘support’. In an ideal world, we would see a line for exactly N31.4 trillion in the liabilities and call it a day for our analysis. But nothing is ever that simple.

Deposits

We have a few suspects to investigate. Deposits of N24 trillion is the most obvious — after all banks typically take deposits from one person and turn it into a loan to another person. Again, we are trying to make a case here that the overdraft money was not printed. Since the money already existed, the CBN simply took it from one person and handed it to the government.

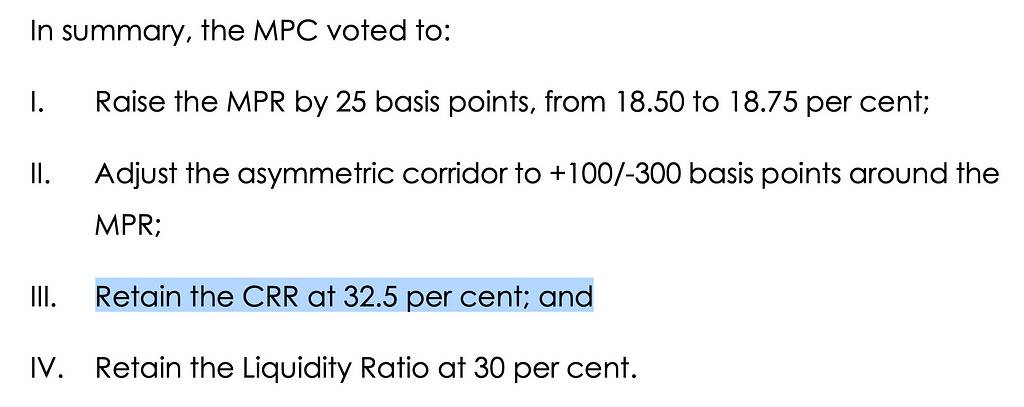

Start with the N11.5 trillion. This is what is known as Cash Reserve Ratio or CRR. This reserve ratio is one of the tools through which central banks can get a grip on the economy and monetary policy in general. Essentially, the CBN can decide that banks must keep a percentage of all the deposits they have ‘on ice’. The idea being that if, say, there is too much money in the economy or things are running hot, the CBN can increase the CRR to cool things down. The larger the ratio, the less money banks have to lend out from their deposits. The money ‘sterilised’ by CRR sits with CBN and it pays a grand total of ZERO percent on it. If the banks don’t like it, they can go to court.

Every quarter when the CBN’s Monetary Policy Committee (MPC) meeting takes place, they announce what the CRR is. Here for instance is from the last meeting held 24–25 July:

That is, if you deposit N100 at the bank, the CBN automatically ‘seizes’ N32.50 from the bank and puts it in a cooler. The bank can only do lending business with the remaining N62.50. This is a perfectly legitimate monetary policy tool. (In reality the CRR works out to a lot more than 32.5 percent for many banks due to the way it's calculated and it can be as high as 50 percent. The reason for this is a bit too complicated to get into but you can think of it as the difference between what you read in a headline and what you end up finding in paragraph 67 of a story, sometimes).

Except that the CBN did not ‘sterilise’ the money to cool the economy. It took it from the banks — which stopped them from lending it to you or your business — and lent it to the government. And as mentioned earlier, it takes the money from the banks, pays them zero percent on it, and then lends it to the government at almost 20 percent. Sweet!

We have to include this CRR money as one of the culprits because there is no way to get to N23 trillion without it. So we have one suspect in the bag. Let’s move on.

Magic Money Recycling

The other thing that jumps out at you in the deposits is the Government deposits. I know you are already going wow wow wow like an ambulance on the way to an emergency. I promise this is going to blow your mind even more.

That’s right — the government, through its various agencies, had N10 trillion sitting as deposits with the CBN (all those TSA accounts). What these accounts are suggesting is that the government was so desperate for money that the CBN was able to package N10 trillion of the government’s own money and lend it to the same government at almost 20 percent interest rate. Sweeter!

This is nothing short of genius and well played to the CBN. We have another suspect in the bag. We are actually almost there as both of our suspects are now worth almost the N23 trillion we are looking for (N11.5 trillion CRR plus N10 trillion deposits). We can ignore the other amounts as they are too small to matter here.

OMO Washes Clean

Just in case the CBN issues a press statement that goes something like ‘we have observed the unwarranted speculation on the social medias about how the CBN funded the overdraft to the Federal Government of Nigeria. Ordinarily we would not have responded to such baseless rumours but…’ and sends us back to square one by denying one of the suspects we have in detention above, we need to tighten our argument by looking for a backup suspect.

The next big item on the liability side of the balance sheet that could have supported N23 trillion in overdraft lending to the government is the Central Bank of Nigeria instruments issued of N14.7 trillion.

We see that this is made up of N10.3 trillion of Open Market Operations (OMO) bills and another N4.4 trillion of ‘Special Bills’. For as long as I can remember — since I was a little boy in Nigeria — I have been hearing OMO as something the CBN uses to ‘mop up excess liquidity’ in the system. You may have heard of the famous quote by the former US Federal Reserve Chair, William McChesney Martin Jr. who said the job of a central banker was to remove the punch bowl before the party gets out of hand. He was talking specifically about interest rates and when to raise them but you can consider OMO as another punch-bowl-removing action.

Basically the CBN takes cash from the banks and gives them a certificate to get their money back in a year or less. The main difference between OMO and CRR is that with CRR, the money never enters into the economy at all (in theory). Once the bank collects the deposit, it hands over the CRR percentage to the CBN. With OMO, the CBN can use it to decrease (or increase) the amount of money already in the system. Ergo, to get the money out of the system, the CBN creates these OMO bills and this time it pays interest on them. From above, you can see that the interest it pays ranges from 3.7–17 percent. The reason for this is that the rate is driven by demand. Say the CBN wakes up tomorrow and decides it wants to ‘mop up’ N100 billion from the system. It goes to the market and says here is N100 billion worth of securities I have to sell, first come, first served. Maybe it does this on a day the banks have so much cash and no one to lend to, so they ‘rush’ the OMO and the CBN receives bids of N200 billion for the N100 billion it wants to sell. In this case demand is far more than supply so the CBN can lower the amount of interest it will pay. (And vice versa for when the supply is higher than demand).

The reason why we have this N10 trillion of OMO as a suspect is straightforward — the CBN gives a certificate to the banks to come back for their money in one year’s time, it takes cash from them in exchange and then lends that cash to the government. That process is logically sound and plausible. The CBN’s effective interest income here will thus be the difference between what it paid the banks as OMO interest and what it charged the government as interest on the overdraft (19.5 percent i.e. the lowest amount it could make would be 2.5 percent being the difference between 19.5 percent charged to the government and the maximum 17 percent it paid on OMO sold to the banks).

Wrinkles

Our 3 suspects now add up as follows — N11.5 trillion in CRR ‘sterilised’ from the banks, N10 trillion of the government’s own deposits and N10.3 trillion of OMO to wash it all down. We now have N32 trillion which is more than enough to cover the N23 trillion we were looking for. But it’s tight — if the CBN issues that press statement denying any one of these suspects, we are automatically below the N23 trillion amount.

Before getting into the wrinkles, you will note that we did not include the N4.4 trillion of ‘Special Bills’ listed under CBN instruments above. This is because after speaking to a couple of people in Nigerian banking who understand these things far better than I do, I understand that these special bills are really part of CRR. To avoid possible double counting, let us leave it out.

Now to our first wrinkle. When I spoke to the aforementioned people who are much smarter than me, I understood that a significant amount of the OMO instruments were actually exchanged for dollars. Remember we concluded in our previous post that the CBN’s sole purpose on earth is now to be chasing after dollars. Nigerian banks sometimes get dollars from their customers and various other sources. The CBN likes to be one in charge of all the dollars in the economy so it often takes these dollars from the banks in the form of a swap arrangement and gives them OMO in exchange. I understand that at the end of 2022, the amount of dollars swapped for OMO in this way stood at $12 billion i.e. N5.5 trillion. We have to deduct this from the possible OMO used to fund the lending to the government otherwise consider the alternative scenario — the CBN writes an OMO bill and takes dollars from the banks which it converts to naira and lends to the government. After a year it has to return the dollars to the banks so it turns the naira back to….no need to go on, it doesn’t make sense. For prudence, let us deduct this N5.5 trillion from the N32 trillion in suspects we have. We still N26.5 trillion which is more than enough to cover the N23 trillion.

The second wrinkle is really a smell test. Accounts are full of words and figures over hundreds of pages. Sometimes they say a lot without saying anything. As far as I’m aware, and in my career as an accountant, there is no law that says one cannot apply common sense when judging numbers presented in financial statements. For the CBN’s accounts, the thing that really requires a common sense judgement is this — how is it that the CBN was able to lend N10 trillion of the government’s own money to it at 19.5 percent interest? We can understand why the CBN might do it given that it needed to find a very large amount of income to cover the expenses in its accounts. But is it possible that no one in the previous government — admittedly led by a simpleton — saw this and said ‘no way’?

The third and final wrinkle is linked to those pesky OMOs. Speak to anyone who works in Nigerian finance and one thing they quickly tell you is that the CBN did not really issue that many OMOs last year (outside of the ones it used as swaps for dollars with the banks). Furthermore, we see from above that its margins on OMO as a funding source are not that large compared with deposits and CRR where it swallows all the margin for itself. Given that the income we are talking about here is N2.3 trillion and the possibility of the OMO margins being as low as 2.5 percent, you will need to a lot of them to generate the levels of income required. This is ultimately another smell test once you combine with the first OMO wrinkle above.

Summary

We have seen that the only way the CBN was able to avoid blowing out its accounts was through a very eyebrow raising and abusive relationship with an incontinent government. The government could not repair its own accounts and was spending far more than it was earning. The CBN was losing a chunk of money chasing after dollars and doing some bad lending. Like 2 crackheads, they met at the home of their dealer and developed a relationship from there. The government avoided judgement day on its spending while the CBN also avoided judgement day on its losses. Win-win for them, lose-lose for Nigeria and Nigerians.

If you have come to this point in the story and you’re disappointed that we don’t really know for sure what has happened after going through nearly 200 pages of words and numbers, all I can say is welcome to my world. A set of accounts is often one of the best places to hide things. The balance sheet balances, the profit and loss delivered a profit and the notes are noted.

Ok but how did the CBN actually fund the government’s deficit?

I don’t know. You tell me.

#TheCBNFiles: Making Money to Spend Money was originally published in 1914 Reader on Medium, where people are continuing the conversation by highlighting and responding to this story.