The Cult of Import Substitution

How a focus on import substitution can be so damaging for a country's development

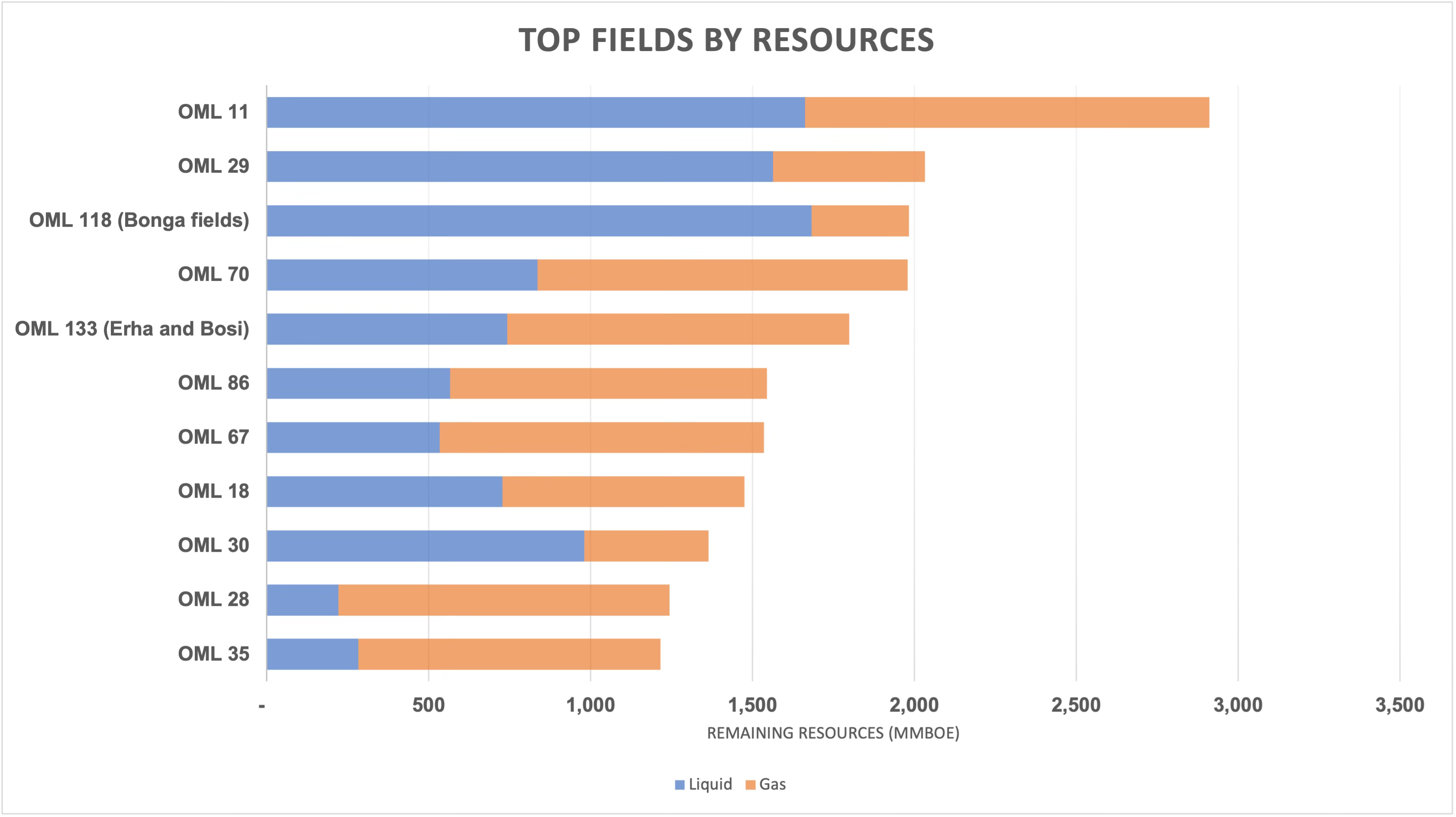

It is always good to start with a chart, so here is one:

We all know Nigeria is currently suffering from low oil production which alarmingly dropped below 1 million barrels per day at a point in 2023. The country has also regularly undershot its OPEC production quota in recent years. The chart above shows Nigeria’s largest oil fields in terms of the remaining resources available to be extracted from them (as of 2024). From this we can quickly conclude Nigeria’s reduced oil production is not because it is running out of oil - there are still billions of barrels in the ground available to be extracted.

What’s happening with the (L)OMLs?

Here are some quick facts about these fields:

OML 11 has been shut in since 1995 at the height of the Ogoni crisis. A story in ThisDay reported earlier this year:

Stakeholders in Ogoniland, Rivers State have declared that for crude oil and gas production to resume in the area, the federal government and operating companies must ensure equity participation for host communities in the area.

OML 29 is now operated by the Nigerian company, Aiteo. It barely produces up to 40,000bpd and it has suffered heavy losses. A recent report in The Cable highlighted this point:

The firm said its oil spill and emergency response team was immediately activated and all production from OML 29 was shut down as a precautionary measure to mitigate the impact of the incident.

As is common with most of the Nigerian companies who bought these assets from the IOCs, Aiteo barely has any money to invest in boosting production and did not even invest anything in the first 2 years after it bought the asset. It is forever suffering losses from leaks and old equipment.

OML 118 is operated by Shell however the company has been delaying investments in the field for over a decade. 3 years ago, an agreement was signed to renew Shell’s operating licence in the hope that it would clear all the legal hurdles that would allow $10 billion worth of investments in the field. That has not happened and it is not hard to link this with the fact that Shell is a company that has been slowly making its way out of Nigeria i.e. it does not look like someone about to put $10 billion in Nigeria.

OML 133 is operated by Exxon Mobil and like 118, its licence was renewed in 2022 for another 20 years. Not much has happened since then other than continued ‘negotiations’. Again, we can make some deductions: Exxon Mobil is busy in Guyana where it has quite literally struck gold and is unlikely to commit the billions of dollars needed to develop the field:

Exxon Mobil discovered a bounty of oil under Guyana’s coastal waters. Soon the company and its consortium partners, Hess and the Chinese National Offshore Oil Corporation, began drilling with uncommon speed. […] The find is projected to become Exxon Mobil’s biggest revenue source by decade’s end.

OMLs 67 and 70 are now 70% owned by NNPC. There’s probably no need to say anything more: NNPC barely has a dollar to its name and definitely does not have the funds to refurbish the ageing platforms on these wells (both of them came on stream in 1970).

OML 18 was taken over by NNPC in March 2023 i.e. it became the operator (LOL). The reasons it gave for taking over the asset from the former operator, Eroton, were that:

While the key business reasons that made the change in operatorship are compelling, it is publicly available information that production has declined from thirty thousand barrels per day (30,000 bpd) to zero. The persisting inability of Eroton to meet the fiscal obligations of the Federal Government led to the sealing of Eroton’s head office in Lagos by the Federal Inland Revenue Service (FIRS) for more than twelve months due to non-payment of outstanding taxes to the Government. Eroton is also not able to remit to the JV parties the proceeds of gas supplied to its affiliate, NOTORE. A number of audits and investigations, including by the EFCC, NURPC’s work programme audit and others have been undertaken or are ongoing. Some of these audits are regulatory steps that may lead to licence revocation under the relevant Laws if drastic steps are not taken by non-operating partners.

If you think NNPC has the money to invest in these assets to bring back their production, kindly give your head a wobble.

OML 86 was bought by NNPC from Chevron in 2021 after it intervened to stop Chevron from selling it to Conoil. It did not even have the money to pay for the purchase and had to rely on a loan from a businessman to get the deal done:

One of Nigeria's wealthiest families, Sayyu Dantata, funded the Nigerian National Petroleum Company Limited (NNPC) purchase of oil blocks from Chevron Corporation, offering an insight into how the firm could back its ambitious expansion plans, a Bloomberg report said yesterday.

A subsidiary of MRS Holdings Ltd provided the NNPC $300 million to buy two shallow-water licenses divested by Chevron, the news medium said, quoting the state-owned company's most recent financial statements.

The transaction was completed in May and the financing is secured against crude from producing fields within NNPC's portfolio, it said.

[…]

The company purchased Chevron's 40 per cent operating stakes in the licenses -- Oil Mining Leases (OMLs) 86 and 88 -- after pre-empting negotiations between the US major and local firm Conoil Producing Ltd. The NNPC is also trying to buy four blocks that Seplat Energy Plc agreed in February to acquire from Exxon Mobil Corp. for $1.3 billion.

This is an example of why NNPC never has any crude to do anything: In this case it has pledged some crude to repay a loan it took to do a deal it had no business doing. It remains unclear what the plan for the assets is.

OML 30 used to be a production big beast. It peaked at over 270,000bpd in the first half of the 1970s (many Nigerian assets peaked in this period). Back in 2018, Shoreline Energy (Nigerian owned) struck a deal with Vitol for $530 million funding to invest in the asset. The plan was to grow production and repay Vitol in crude oil:

European trading house Vitol has reached a $530 million deal with Nigeria's Shoreline to finance an oilfield in exchange for access to some of the 50,000 barrels per day (bpd) of oil it produces, the Nigerian company said on Thursday.

[…]

The agreement with Shoreline, finalised on Thursday, will provide the company with cash to refinance existing debt and further develop OML 30 in Nigeria's oil-rich Delta region.

The field currently produces 50,000 bpd and has an estimated 1 billion barrels of oil reserves. Shoreline has a 45 percent interest in the field.

Shoreline chairman Kola Karim said the "transformational" deal would enable the company to step up gross production to as much as 100,000 bpd over the next year.

That 100,000 bpd of course never happened. According to the NUPRC annual report, the field was only expected to produce 33,000 bpd as at the end of 2023 (Page 17).

OMLs 28 and 35 are doing well relative to the others. Both have large quantities of gas and Shell remains invested in them. OML 28 includes the Gbaran-Ubie gas field which had a fire outbreak a couple of months ago but was swiftly contained. Here’s how it was described at the time:

The Gbaran facility, which began operations in 2010, is by far the most important Nigeria LNG gas feedstock project, processing almost 2 billion standard cubic feet of gas per day.

To summarise, 8 out of 10 of Nigeria’s top assets are suffering serious issues and grossly underperforming. Selling the assets to Nigerians has yielded practically no benefits whatsoever as they have found it almost impossible to mobilise the funding needed for investments. And the less said about NNPC the better.

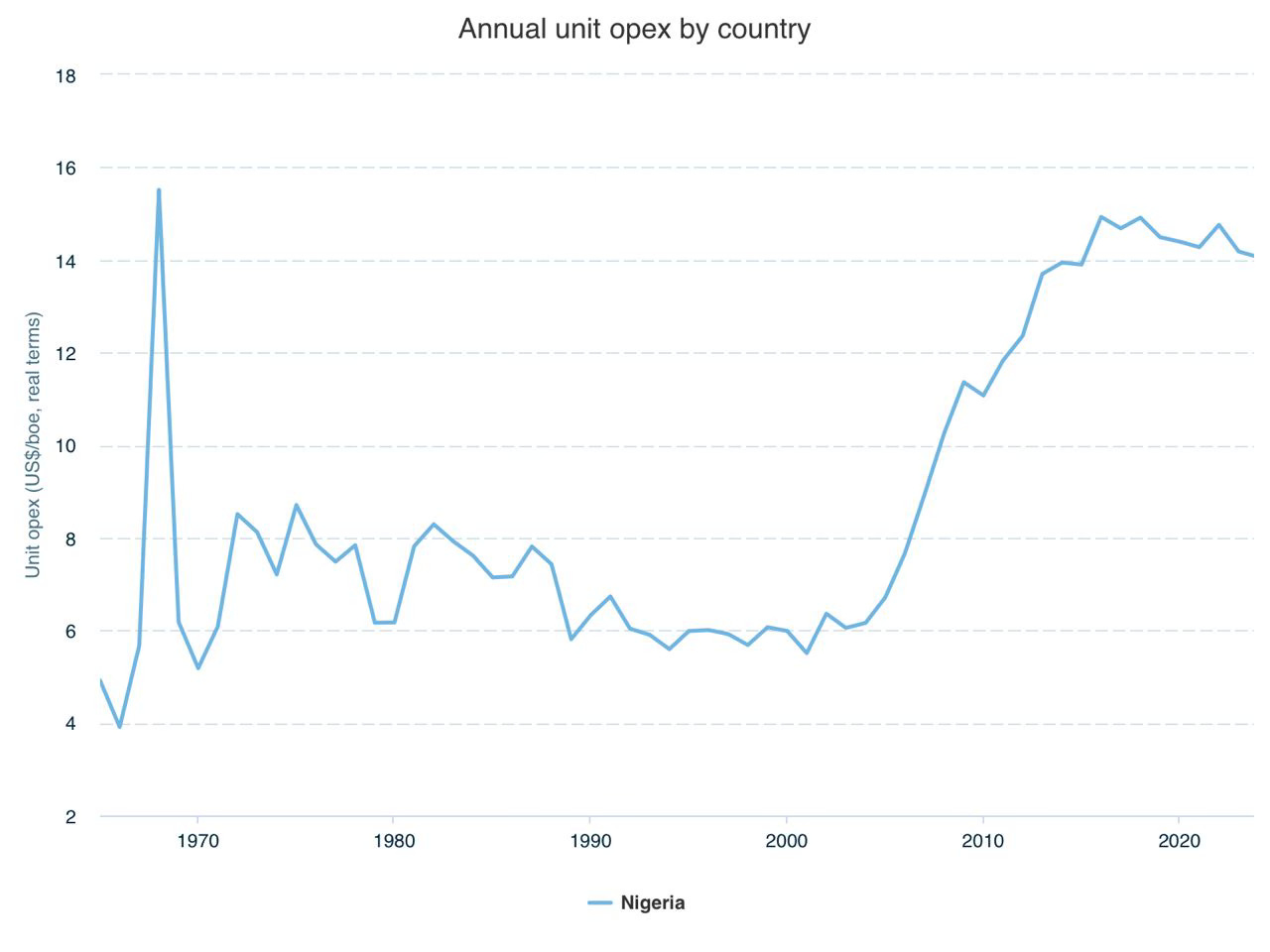

One way to summarise all of the above is with the chart below:

Nigeria’s operating expenses per barrel is now back where it was in the late 1960s for the simple reason that costs are now being spread over fewer and fewer barrels of oil.

Nigerian or African problem?

But what’s going on elsewhere? Is this a Nigeria or Africa-wide problem? Let’s do a quick tour.

In 2020, Petrobras exited Nigeria and this was taken as it effectively leaving Africa as it had no assets anywhere else on the continent:

Brazil’s state-controlled oil company Petroleo Brasileiro SA has finalized the sale of its shares in Petrobras Oil & Gas B.V. (PO&GBV), the company producing oil in Nigerian oil assets, thereby ending its activities in Africa.

The Brazilian state-controlled firm had 50 percent of the company, in a joint venture with BTG Pactual E&P B.V, and sold its shares to Canada’s Africa Oil Corp. for $1.45 billion.

BTG, Brazil’s largest independent investment bank owns the other 50percent stake in Petrobras Africa, whose core assets are stakes in offshore fields that produce Nigerian oil grades Agbami, Egina and Akpo.

But Petrobras is back in Africa. At the start of this year, it announced its entry into 3 oil fields in Sao Tome & Principe, right on Nigeria’s doorstep:

Petróleo Brasileiro SA (Petrobras) has closed a deal to acquire interest in three exploration blocks offshore Africa from Shell plc.

After signing amendments to the production sharing contracts and joint operating agreements, Petrobras has joined the consortia for blocks 10, 11, and 13, in São Tomé and Príncipe, Africa.

Shell is operator of all three blocks with 40% interest. Partners in Block 10 are Petrobras (45%) and ANP-STP (15%). Partners in Block 11 are Petrobras (25%), Galp (20%), and ANP-STP (15%). Partners in Block 13 are Petrobras (45%) and ANP-STP (15%).

This really should be sobering for Nigeria and ought to trigger alarm bells given that Petrobras is a fairly aggressive investor across the world. A couple of days ago, it was announced that Petrobras was bidding for a $4 billion oil asset in Namibia.

Also a couple of days ago, an Exxon Mobil drillship arrived off the coast of Angola and Namibia:

ExxonMobil is about to spud a long-awaited deepwater wildcat in the frontier Namibe basin offshore Angola.

If the US giant strikes big oil with its Arcturus-1 probe in Block 30, it will be a huge boost for one of Africa’s long-neglected plays, opening up a new exploration frontier in a basin that extends into northern Namibia.

Drillship Valaris DS-9 arrived at location on 23 July and appeared to be preparing to spud ExxonMobil’s wildcat, according to marine intelligence provider VesselsValue.

Technip and JGC have been working closely with ExxonMobil on Rovuma LNG since 2019 when, together with Fluor, they were chosen to design and build what was then a 15.6 million tpa LNG plant expected to cost some $24 billion

We can go on and on. The point is to say that it is still possible to obtain large investments in oil and gas in Africa and a lot of the struggles Nigeria is facing are unique to Nigeria.

The chokehold of import substitution

Given how long it takes to actually get oil out of the ground after investing billions of dollars, it is safe to say that Nigeria’s short to medium term future as an oil producer is already fixed i.e. current levels of production will steadily decline while the country struggles to replace the lost foreign exchange earnings from crude sales.

How did Nigeria get here? How did the country allow one of its most valuable gifts from God to essentially decay in this manner?

A thesis can be written on the answer but the under-discussed culprit I want to focus on here is the cult of import substitution. This cult has had Nigeria in a chokehold (as the kids say) for decades now to the point where you can pick an intellectual or an agbero and you will find believers among them. The simple message of the cult is that if Nigeria is spending money to import something, that is a loss and as such investment must be directed towards replacing those imports. This idea has been so throughly entrenched in Nigeria, it is not controversial at all to say it and you will be looked at like a crazy person if you try to challenge it.

The grand culmination of the cult of import substitution is the Dangote Refinery sitting in Lagos, Nigeria. Twenty billion dollars was mobilised into this investment to replace the imports of petrol into Nigeria, probably the largest single investment in anything in Nigerian history. At a point, Nigerian banks were fighting to be part of the deal to lend Dangote the money to fund the refinery’s construction. Dangote of course mobilised several billion himself from his cement empire, which was itself another iteration of the cult of import substitution. Nigerians have tolerated obscenely high cement prices for decades and made a cement seller a dollar billionaire because it was the cult of import substitution made flesh.

Every investment need or requirement comes second to the cult of import substitution. Nigeria is crying out for investment in education to improve its human capital so that the country can be prepared for an imminently arriving future. The country is crying out for investments in infrastructure, energy, healthcare and everything else that can make a society worth living in and a place that gets the best out of its citizens. You could never mobilise $20 billion worth of investments into any of these things. But a refinery?

As crude oil is already in Nigeria and does not need to be imported, the cult of import substitution cannot ‘see’ it. OML 67, as an example, is one of the largest ever fields discovered in Nigeria. At one point just before the turn of the millennium, it was producing an incredible 430,000 bpd of oil. By 2015 it had consumed $16 billion worth of capital expenditure to get all that oil flowing. Exxon Mobil who spent all that money on it have since got bored and, as we discussed above, are distracted with their eyes elsewhere. Today that field is struggling to do even 50,000 bpd. The cult of import substitution, ironically, does not notice capital importation.

One might say these things are not mutually exclusive or at least they shouldn’t be: you can have investments in education and also have a refinery. In theory, yes. The trouble with the cult of import substitution is that it is always looking backwards and so it cannot see anything that requires looking forward like education. In the near future, something is going to be invented somewhere outside of Nigeria that will improve the lives of Nigerians. They will then start importing that thing in large quantities and it will then become ‘interesting’ to invest in replacing those imports into Nigeria. But actually investing in those things before anyone can see what they look like? No chance.

There is of course a case to be made for import substitution but it cannot be allowed to be the decision tree for any and all investments. Everyone now believes the point of a giant refinery in Lagos is to stop importation of fuel and ‘save’ Nigeria the foreign exchange it is spending on those imports. But why is the justification never that a refinery can and should be a tool for Nigeria to earn more foreign exchange through exports?

The cult of import substitution leads a country down damaging roads. It blinds it to what investments are actually needed to secure its future. It is forever looking backwards and never forward.

And perhaps worst of all, it prioritises investment in refining while the actual crude to be refined slowly dries up due to lack of investment.

This is a "luku and lafu" situation......the most obvious reason why these Nija companies are non-performing is IMHO, (1) None of these people that got the licenses ever had the capacity, capability, knowhow, integrity nor even the requisite ability to own/operate these platforms. All they were doing was just "man know man", and once the licenses were acquired, then used agbero principles to source for partners (incompetently) I might add...and once they collect some upfront monies from said partners, throw a few parties and destination weddings wherever or buy shitty real estate out here in the west, the partners (who are usually just are obviously rapacious bizmen themselves) can tell/know Nigerians are full of it. Why else would these investors go to other African countries to make money??? Money is money, is money afterall and I guess this leads me to the (2nd) thing, which is that we would never succeed using our reserve/backup team. I just saw a pix where some Nigerians went to a meeting in China(no idea what it was for, but my guess is, they went to beg China for some more money, shameless idiots).....the Chinese side of the table was 3 deep (about 18 or so people) and they all had their ipads and laptops opened.....the Nija side was about 6 people, all in their immaculately starched guinea brocade(that was probably made with Nigerian/African cotton but ginned in China/Bangladesh and re-exported back to Nija as a finished product) with 2 or 3 cellphones(also made in China) each all on the table beside them, (probably lol)wondering when they were taking the next break to go eat....SMH

Unfortunately people don't seem to understand this. It's a weird fantasy we have. Even the US with it's industrial might doesn't manufacture everything but some how people here think it's possible. They outsource manufacturing to Asia because of it's cheap to make it there.